Business

Column: Hedge funds eye U.S. bond boost after bruising Q1,

ORLANDO (Fla.), April 11, 2011 (Reuters) – The first quarter of the U.S. bond markets was marked by high volatility and the worst performance in decades. Hedge funds had a poor quarter and will hope for a better second quarter.

U.S. futures markets positioning for the first week in the new quarter showed that funds were generally correct on the move up short-dated rates or yields but did not anticipate the rise in the 10-year yield.

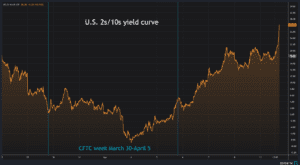

It was mixed on the relative value trades between two-year Treasuries and 10-year Treasuries, as well as the closely monitored “2s/10s” yield curve. But the curve flattening funds were positioned for did not come to pass until a very short time.

Data from the Commodity Futures Trading Commission showed that funds reduced their short-term 10-year Treasuries position by 113,682 to 362,875 while increasing their short work in 2-year bonds to 72.194 contracts 59,202.

It was a wager on the 10-year yield declining and the 2-year yield rising.

The 10-year yield jumped to 2.55% from 2.40% during that week. It has continued to rise, reaching 2.77% on Monday. In the week ending April 5, the two-year cash yield increased by 30 basis points to 2.60 percent.

A short position is a bet that an asset will lose value, while a long post is a wager to rise. Bond yields increase when prices fall and decrease when prices rise.

These CFTC position changes were a collective bet that the curve would be flatter than “2s/10s”. On April 4, the angle was inverted by eight basis points before quickly steepening to +20bps a few days later.

Q1 CURVE CRUSHED

Hedge funds are known for taking long-term directional wagers and maximizing arbitrage opportunities that arise from rising volatility. Although funds did seem to have it all right by the beginning of the second quarter, their Treasuries bets were extremely difficult.

HFR, a data provider for the industry, said Friday that its Relative Val Fixed Income-Sovereign Index suffered a 2.66% loss in the first quarter. This is a shocking contrast to the 7.71% increase in its wider Macro Index. Continue reading

Comparing the shifts of CFTC Treasuries futures position in the January-March period to moves in U.S yields shows funds got the directional wagers on higher yields right but lost on their curve trades.

Funds increased their 10-year bond net position by nearly 265,000 contracts and their 2-year net work by 147,000 contracts, effectively betting that the 10-year yield will rise more than the 2-year yield.

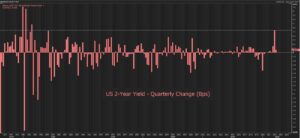

The quarter saw a 3% increase in the 10-year yield to 83 bps. However, the work for the two years jumped 160 bps to record the largest quarterly gain in more than 40 years. The curve flattened by an average of 77 bps since 2011.

There is an overwhelming consensus that the Fed will soon engage in the most aggressive policy tightening since the 1930s via dramatic interest rate increases and rapid reductions of its balance sheets. Continue reading

Where does this curve take us?

Citi analysts note that a substantial amount of easing has already been priced into the U.S. money market from the expected peak of rates in the second quarter. This suggests there is little room for the curves to flatten further.

Morgan Stanley analysts argue that the inverted yield curve is here to stay without necessarily indicating a recession.

Funds will hope they are on the right track if a clear trend is apparent over the quarter.